I've been evaluating North Finance since last week. I cannot seem to figure out how they calculate overnight swaps. When I ask their support, they always refer me to http://www.northfinance.com/eng/cfd/...rex-contracts/ but it does not explain the calculations involved. I've asked their email support and "Live" support, and they basically cycle around pointing you to the link above and seem unable / incompetent to calculate it either.

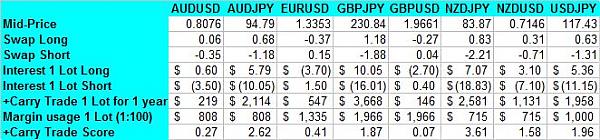

I've tested a GBPJPY 1 day swap on a 0.1 lot LONG. The table says 1.18 "points", but the [Trade] and [Account Activity] show 1.00. I wasn't sure that mean "number of base swaps", or what? But now that I've closed 2 swapped trades, it appears to be crediting 1USD per day per 0.1 lot LONG!?

I cannot retrace the calculation based on the formula I was given:

Swap Rate Point * 1000

- - - - - - - - - - - - - - - - - * Lot Size

Base currency rate

http://img164.imageshack.us/img164/3...board01jm2.jpg

I've tested a GBPJPY 1 day swap on a 0.1 lot LONG. The table says 1.18 "points", but the [Trade] and [Account Activity] show 1.00. I wasn't sure that mean "number of base swaps", or what? But now that I've closed 2 swapped trades, it appears to be crediting 1USD per day per 0.1 lot LONG!?

I cannot retrace the calculation based on the formula I was given:

Swap Rate Point * 1000

- - - - - - - - - - - - - - - - - * Lot Size

Base currency rate

http://img164.imageshack.us/img164/3...board01jm2.jpg