DislikedA really nice and helpful "feature" would be to post a screenshot of a random day of your chart for the currencies you talk about in the above post so we can match our TMA values accordingly. Thank you for the work you are putting into this thread. I will write more during the weekend as I am busy at the moment. Do you always re adept your your rules? (You are done with a month take a look at the past 6 months and take the best settings and do this month after month after month?) Or did you decide on this values back in 2012 and you have never touched...Ignored

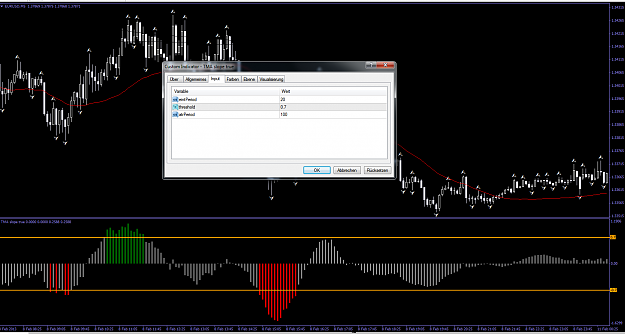

Now another helpful thing is that TMA is not going to be lower then mine so if I said GBP/USD TMA is 0.33 +/- its Not going to be lower then that your Not going to be looking for 0.23 +/- TMA.

So might have to look higher but you don't look for to high TMA.. Such as If TMA is 0.33 +/- your not going to look for 0.5 +/- TMA or higher.. It will only deviate by a little from mine so you might go into 0.4 +/- Area maybe even as high as 0.45 +/- but that's it and same general idea with the rest of them.

So just the process of elimination helps narrow down accuracy and once you find that level -- that works properly that's it.

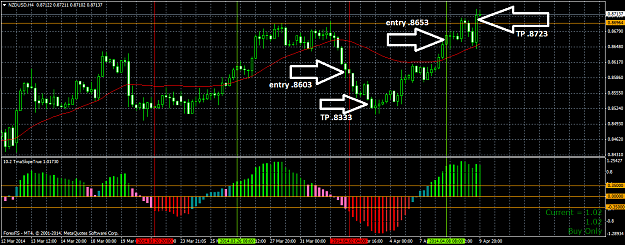

Just quoting your question: Do you always re-adept your rules?

When starting out.. you re-adept so for example.. Lets say.. I start with 0.4 but as I'm going along I see well I can bring it down to 0.37. Once you find the best setting, that's it there is no more re-adept and changing. It just once you tweak and narrow it and find the right setting the best setting, it stays the same.

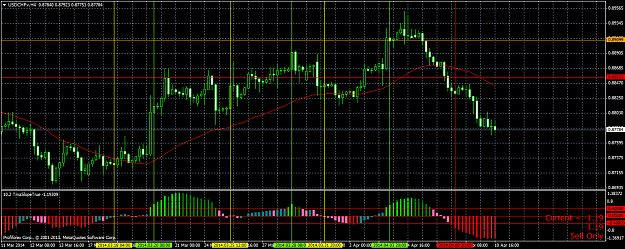

The difference between this system and others system.. Back-testing is as good as forward testing.. AS long as you take it objectively and unbiasedly. What I mean by that is.. Lets say we started from Last month or January when we look at the chart its just a recording of what has already happened, now we can watch it happen an unfold and it won't change that result it'll still be the same if we didn't watch it.

What we must do though is use the EXACT same way of taking a trade during that point where we watch the trade unfold as when we collect back test data and we already see what happened.. But if you back-test with the objective idea in mind that hindsight does not exists.. So like you don't know what is going to happen, so you need to make sure that you only collect data that is available at the entry point ANYTHING else beyond that goes into the measurement and obviously is static the only dynamic is the entry, and the dynamic entry has to be replicable so what we do in previous date has to be able to do in our current data like today.

By doing that, previous data is the same as current data only difference is the patterns that we analyze. Now there is a lot of things that go into patterns not only wins and losses.

But how many trades per month.. How many longs how many shorts? What is the average length of the trade.. Its a lot of data that makes patterns and when we follow this patterns we get a picture when we enter into a trade today.. We already know EVERYTHING to expect.. We know the range, we know the average ranges, we know the highs and the lows -- we know the length of the trade.. So it clears a lot of the ambiguity of trading.. Where you have a level of confidence and knowledge and takes stress off trading.

Of course there is always curve balls, but you got GBP/USD trade that was lost its okay you knew it could happen you planned for it, you had safety net and exit and everything.

There are those who know, and there are those who don't know.