Hi all.

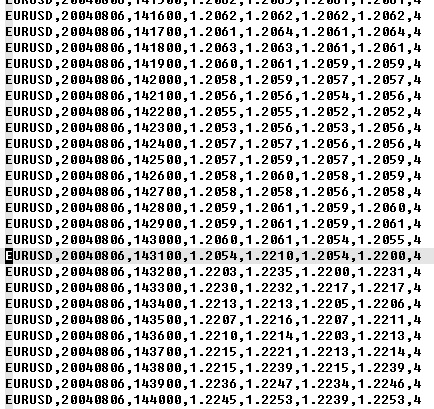

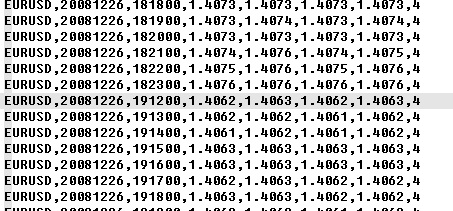

I have recently written a simple MQL script for the only purpose of testing the historical data of Metaquotes. Basically, it simply spans the whole historical data of a given pair, checks if there are data gaps in the time and price domain and then writes a text report. The results tell that the quality of the data is really poor. This means that with this data the result of any kind of backtest is completely erroneous, even for long term strategies. Anyone dealing with such issue?

I have recently written a simple MQL script for the only purpose of testing the historical data of Metaquotes. Basically, it simply spans the whole historical data of a given pair, checks if there are data gaps in the time and price domain and then writes a text report. The results tell that the quality of the data is really poor. This means that with this data the result of any kind of backtest is completely erroneous, even for long term strategies. Anyone dealing with such issue?