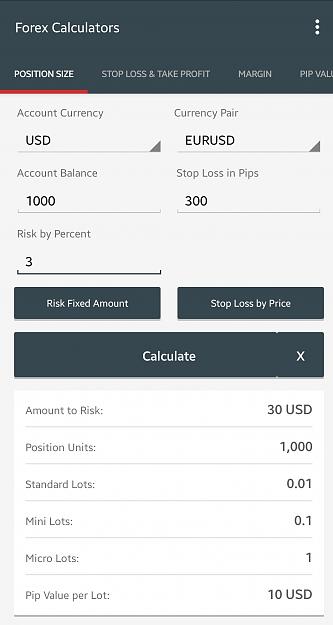

So, I know this topic has been beat to death. So I'm here to beat it up some more.

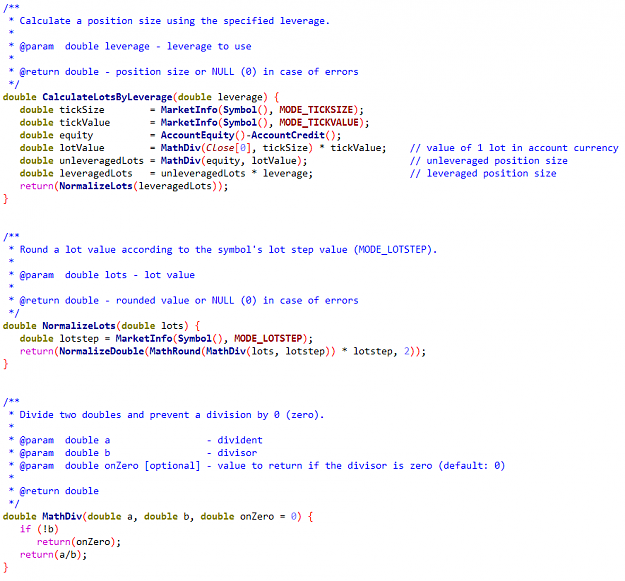

Given the following formula:

Lot=((Account_Balance*Risk_Percentage)/100)/(StopLoss*tickvalue)

Given these values:

Account_Balance=1000

Risk_Percentage=3

StopLoss=300

tickvalue=1

I get a value of 0.1. Now, that's great if I'm on a micro account (10,000 units=1 lot). But if I'm on a standard account (100,000 units = 1 lost) then the calculation is off. So, how does lot size play into this calculation? Right now it doesn't, and it should.

Note: assume 5 digit broker, thus 300 pip stop loss. Also USD dollar account and trading a USD pair; thus tickvalue=1

Given the following formula:

Lot=((Account_Balance*Risk_Percentage)/100)/(StopLoss*tickvalue)

Given these values:

Account_Balance=1000

Risk_Percentage=3

StopLoss=300

tickvalue=1

I get a value of 0.1. Now, that's great if I'm on a micro account (10,000 units=1 lot). But if I'm on a standard account (100,000 units = 1 lost) then the calculation is off. So, how does lot size play into this calculation? Right now it doesn't, and it should.

Note: assume 5 digit broker, thus 300 pip stop loss. Also USD dollar account and trading a USD pair; thus tickvalue=1