Prop Firm DrawDown Protector : Prop Firm Capital Protection Expert MT5 |Forex Money Management: Forex Trade Management Expert MT5 | ICT Concepts Indicator MT5 |Smart Money Concepts Expert MT5 | Smart Money Trap Scanner | Get a free Expert Advisor license via Telegram and WhatsApp

The Historical Evolution of Interest Rates

The concept of interest is among the oldest financial instruments, with documented use in ancient Sumer, Babylon, and Egypt. While Greek philosophers like Aristotle criticized it, and medieval religious doctrines often forbade it as usury, the necessity for trade and development persisted. The Renaissance and the rise of modern banking formalized its acceptance. Today, central banks wield the Interest Rate as a primary monetary policy tool to manage inflation, stimulate growth, and ensure financial stability.

Why are Interest Rates So Important?

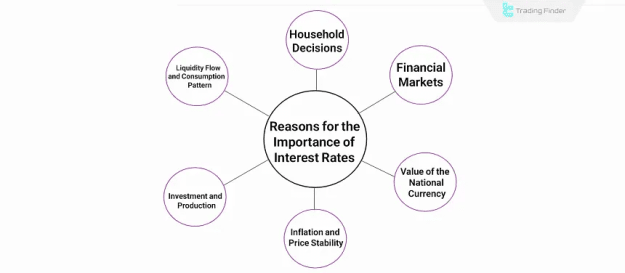

As the price of money, interest rates are a pivotal macroeconomic variable with far-reaching consequences:

- Capital Allocation & Consumption: They direct the flow of liquidity in an economy and shape spending versus saving decisions.

- Business Investment: Lower rates reduce financing costs, making capital projects and expansion more attractive for companies.

- Inflation Control: Central banks raise rates to cool an overheating economy and curb inflationary pressure.

- Currency Valuation: Rate differentials between countries drive foreign investment flows, directly impacting exchange rates.

- Financial Market Dynamics: Rates determine the attractiveness of bonds, savings accounts, and influence capital movement into or out of equity markets.

- Household Finance: Decisions regarding mortgages, savings, and consumption hinge on the prevailing interest rate environment.

Core Types of Interest Rates

Understanding the calculation method is essential, as it drastically changes the total repayment or return.

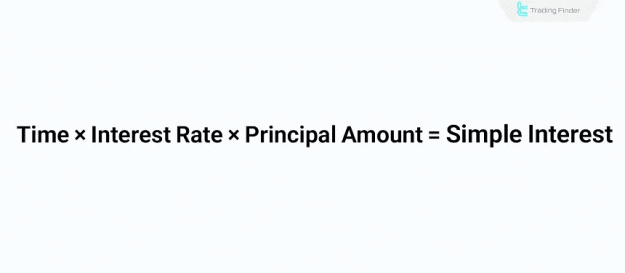

Simple Interest Rate

Simple interest is calculated only on the original principal amount throughout the loan or deposit period. It does not compound.

- Formula: Simple Interest = Principal × Interest Rate × Time

- Example: A $1,000 deposit at 10% simple annual interest yields $100 each year, totaling $300 after three years.

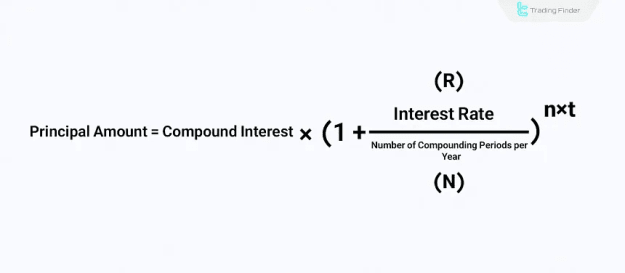

Compound Interest Rate

Compound interest is applied to the principal and the accumulated interest from previous periods, leading to exponential growth.

- Formula: Future Value = Principal × (1 + Interest Rate/Compounding Periods)^(Periods × Time)

- Example: $1,000 at 10% annual interest, compounded annually, grows to $1,331 after three years. The $31 difference from the simple interest example illustrates the powerful "interest on interest" effect.

Fixed vs. Variable Rates

- Fixed Rates: Remain constant for the loan's duration, providing payment predictability and protection against future rate hikes.

- Variable (Floating) Rates: Fluctuate based on a benchmark rate. They may offer lower initial costs but carry the risk of higher payments if rates rise.

Interest Rates as a Monetary Policy Tool

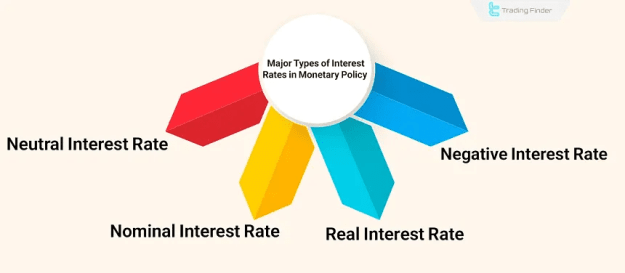

Central banks use various rate concepts to steer the economy.

- Nominal Interest Rate: The official, stated rate set by a central bank.

- Real Interest Rate: The nominal rate minus inflation. A positive real rate is restrictive, while a negative real rate is stimulative.

- Negative Interest Rate: An unconventional policy where depositors pay to hold money with a bank, aimed at discouraging saving and stimulating spending/investment during deflationary risks.

- Neutral Interest Rate: The theoretical rate that supports the economy at full employment without stoking inflation. It serves as a key benchmark for policymakers.

The Impact of Interest Rates on Financial Markets

Rate changes are a primary driver of market sentiment and asset prices.

- Expansionary Policy (Rate Cuts): Lowers borrowing costs and returns on safe assets. This typically boosts risk-on assets like stocks and cryptocurrencies as liquidity increases and financing becomes easier. Historical charts of indices like the S&P 500 often show upward trends following cutting cycles.

- Contractionary Policy (Rate Hikes): Increases the cost of capital and yields on bonds. This tends to dampen economic activity and can lead to outflows from riskier markets as investors seek safer, higher-yielding returns.

- Forex & Global Trade: Countries with higher relative interest rates often attract foreign capital, strengthening their currency. This can make exports more expensive and imports cheaper, affecting trade balances.

- Gold: Often behaves as a hedge; its price may rise during rate-cut cycles due to a weaker fiat currency outlook, though its safe-haven nature can lead to less dramatic moves compared to equities.

Tracking Interest Rate Decisions

Traders monitor economic calendars for key central bank announcements and data releases (inflation, employment) that influence rate expectations. Tools like the Forex Factory Calendar indicator can be integrated into trading platforms to visualize high-impact news events directly on charts, helping traders anticipate market volatility.

Advantages and Disadvantages of Different Rate Structures

- Fixed Interest Rate

- Advantages: Predictable payments, protection against rising rates.

- Disadvantages: No benefit if market rates fall; often higher initially than variable rates.

- Variable Interest Rate

- Advantages: Potential savings if market rates decrease; lower initial cost.

- Disadvantages: Payment uncertainty, risk of higher costs if rates rise.

- Simple Interest

- Advantages: Straightforward calculation, transparent for short-term loans.

- Disadvantages: Does not maximize returns on long-term investments.

- Compound Interest

- Advantages: Maximizes long-term returns for investors; leads to exponential growth.

- Disadvantages: Increases the debt burden for borrowers over long periods.

Conclusion

The Interest Rate is far more than just the cost of a loan; it is the cornerstone of modern monetary policy and a dominant force in global finance. Its level and direction shape economic growth, currency values, and the performance of every major asset class. Whether you are an investor, a business owner, or a consumer, understanding the mechanics and implications of interest rates—from simple vs. compound to the intent behind central bank policies—is essential for making informed financial decisions in an interconnected world.