-

XAUUSD: Elliott wave analysis and forecast for 19.04.24 – 26.04.24

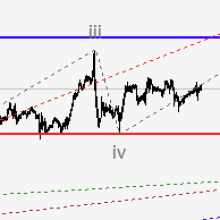

Main scenario: consider long positions from corrections above the level of 2324.77 with a target of 2450.00 – 2500.00. Alternative scenario: breakout and consolidation below the level of 2324.77 will allow the pair to continue declining to the levels of 2154.83 – 2019.86. Analysis: a descending correction appears to have formed as the fourth wave (4) of larger degree on the daily chart. The fifth wave (5) is unfolding, with first wave 3 of (5) forming as its part. Apparently, the third wave of smaller degree iii of 3 is forming on the H4 time frame, with wave (iii) of iii developing inside. Wave iii of (iii) is ... (full story)

- Comments

- Subscribe

-

- Older Stories

From ecb.europa.eu|Apr 19, 2024

From ecb.europa.eu|Apr 19, 2024Since our last meeting in October, the global growth outlook has improved somewhat, reflecting revised growth prospects across both advanced and emerging market economies. The disinflationary process has continued amid falling energy prices, the normalisation of supply conditions and tight monetary policy. While the global economy has weathered the tightening of monetary policy well, growth prospects remain subpar by historical standards. Risks to the global outlook are broadly balanced for both economic activity and inflation, though rising geopolitical tensions pose an upside risk to inflation and a downside risk to growth. post: ECB'S PRESIDENT LAGARDE: THE DISINFLATION PROCESS IN THE EURO AREA HAS CONTINUED. post: ECB’s Lagarde: if Inflation Criteria Met, It Would Be Appropriate to Reduce the Current Level of MonPol Restriction ECB’s Lagarde: at the Same Time, the Governing Council is Not Pre-Committing to a Particular Rate Path post: ECB'S PRESIDENT LAGARDE: IF THE INFLATION CRITERIA IS MET, IT WOULD BE APPROPRIATE TO REDUCE THE CURRENT LEVEL OF MONETARY POLICY RESTRICTIONS.

From vaneck.com|Apr 19, 2024

From vaneck.com|Apr 19, 2024Geopolitical conflict and the specter of ongoing weakness in the Chinese economy continued to have an outsized impact on commodity prices for most of the quarter. Persistent ...

From cnbc.com|Apr 19, 2024|5 comments

From cnbc.com|Apr 19, 2024|5 commentsIran and Israel, regional arch-foes, are trading attacks and threats — the latest of which saw Israel launch a “limited military strike” on Iran in the early hours of Friday ...

-

- Newer Stories

From tmz.com|Apr 19, 2024

From tmz.com|Apr 19, 2024Ryan Garcia will live up to his King Ry moniker Saturday night in NYC ... 'cause the star boxer commissioned an insane iced-out crown -- with over 15,000 diamonds -- that he plans ...

From forexlive.com|Apr 19, 2024

From forexlive.com|Apr 19, 2024The IMF European regional report is out and says: • Soft landing for European economies is in reach but not assured - • High-debt European economies should consolidate fiscal ...

From chicagofed.org|Apr 19, 2024

From chicagofed.org|Apr 19, 2024video The U.S. economy made substantial progress in 2023 on the Federal Reserve’s dual mandate of maximizing employment and stabilizing prices. Inflation had one of the largest drops in the last 50 years and did so with solid growth, low unemployment, and no recession. So far in 2024, that progress on inflation has stalled. You never want to make too much of any one month’s data, especially inflation, which is a noisy series, but after three months of this, it can’t be dismissed. I am still hopeful that we will again see a return to improvement on inflation in the months ahead, as our restrictive monetary policy continues to curb inflation pressures and the economy continues returning to pre-pandemic norms. At the end of the day, we will get inflation back to target. I always say that the first rule for data dogs is that when you are uncertain, keep sniffing. Right now, it makes sense to wait and get more clarity before moving. We were at our 2 percent target before Covid, but not because inflation of everything was 2 percent.. Housing was around 3.5 percent, services 2.5 percent, and goods –1 percent. Much of the improvement in inflation last year came from positive supply developments. As the supply chains healed, goods inflation returned basically back to pre-Covid rates. Most of that supply healing is now complete. Part of the supply side benefit last year came from increases in labor supply, in part from immigration and in part from higher participation rates of many groups. The impact of that will likely continue to help the economy this year. While we saw deterioration in services inflation last month, there was surprising improvement over the course of 2023—it remains above pre-Covid trends, but there may be more space for progress. That leaves the main short-run problem as I see it, which is persistently high housing inflation—still much higher than it was pre-pandemic. Looking at market data on rents for new leases, I’d say housing inflation is supposed to have been falling. If it doesn’t, it will be hard to see a smooth path back to our 2 percent inflation goal. As we have seen strong gross domestic product (GDP) and jobs numbers, we need to determine if this is a sign of overheating driving up inflation. But let’s be careful: As I have said before, when there are supply side developments (for example, higher productivity growth, supply chain improvements, or increasing labor force participation or population growth), aggregate numbers are not great measures of overheating. There are crosscurrents at work. Not all the data s post: Goolsbee: Proper Fed Policy Going Forward Will Depend on the Data Goolsbee: Fed’s Current Restrictive MonPol ‘Appropriate’ Goolsbee: ‘Makes Sense to Wait’ to Get More Clarity Before Moving Fed’s Goolsbee Says Progress on US Inflation Has Stalled post: Goolsbee: Still Hopeful for Return to Improvement on Inflation in Months Ahead Goolsbee: Persistently High Housing Inflation’s Main Short-Run Problem Fed’s Goolsbee: We Have to Recalibrate, We Have to Wait and See post: ? GOOLSBEE: THE GOLDEN PATH IS MORE DIFFICULT FOR 2024 ? GOOLSBEE SAY REAL FED FUNDS RATE IS HISTORICALLY QUITE HIGH ? GOOLSBEE: THE POLICY TRADEOFFS ARE HARDER THIS YEAR post: Fed's Goolsbee: Unproductive Speculating On Conditions For Raising, Or Cutting, Rates - Determining Policy Restrictiveness Depends On The Data

- Story Stats

- Posted: Apr 19, 2024 9:16am

- Submitted by:Category: Technical AnalysisComments: 0 / Views: 208