-

Gold firmly above 50-day, 200-day moving averages; 3/27/24

Gold futures remain firmly above 50-day and 200-day moving averages. Phillip Streible examines the continued strength in the precious metal.

- Comments

- Subscribe

-

- Older Stories

From mining-technology.com|Mar 27, 2024

From mining-technology.com|Mar 27, 2024When we talk about minerals that are essential for our modern world, uranium often finds itself in the spotlight. As the world turns its attentions towards nuclear power as a ...

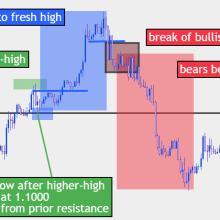

From forex.com|Mar 27, 2024

From forex.com|Mar 27, 2024In the last price action installment, we looked at how traders can analyze a chart without any indicators, focusing solely on a market’s price structure to help with trading ...

From @financialjuice|Mar 27, 2024|3 comments

From @financialjuice|Mar 27, 2024|3 commentspost:

RBNZ'S GOVERNOR ORR: I SEE SIGNS FOR “MORE NORMALIZED" RATES ON THE HORIZON.

RBNZ'S GOVERNOR ORR: I SEE SIGNS FOR “MORE NORMALIZED" RATES ON THE HORIZON.

-

- Newer Stories

From bnnbloomberg.ca|Mar 27, 2024|2 comments

From bnnbloomberg.ca|Mar 27, 2024|2 commentsDaniel Kahneman, a psychologist whose work casting doubt on the rationality of decision-making helped spawn the field of behavioral economics and won him a Nobel Prize, has died. ...

From federalreserve.gov|Mar 27, 2024|8 comments

From federalreserve.gov|Mar 27, 2024|8 commentsThank you, Barbara, and thank you for the opportunity to speak to you today. My subject, as it often is, is the outlook for the U.S. economy, and how that affects the Federal Open Market Committee's (FOMC) continuing effort to reduce inflation to a sustained level of 2 percent while maintaining a healthy labor market. We made a lot of headway toward our inflation goal in 2023, and the labor market moved substantially into better balance, all while holding the unemployment rate below 4 percent for nearly two years. But the data we have received so far this year has made me uncertain about the speed of continued progress. Back in February, I noted that data on fourth quarter gross domestic product (GDP) as well as January data on job growth and inflation came in hotter than expected. I concluded then that we needed time to verify that the progress on inflation we saw in the second half of 2023 would continue, which meant there was no rush to begin cutting interest rates to normalize the stance of monetary policy. Over the past month, additional economic data has reinforced this view. February job gains moved back up to 275,000, making the three-month average a strong 265,000, and various inflation measures have continued to come in hot. Core personal consumption expenditures (PCE) inflation jumped to 0.4 percent on a monthly basis in January, after averaging around 0.1 percent in October through December last year. And with February consumer price index (CPI) and producer price index inflation data in hand, some forecasts are predicting core PCE inflation may be revised up for January and is expected to come in at 0.3 percent for February, which we will learn about on Friday. Adding this new data to what we saw earlier in the year reinforces my view that there is no rush to cut the policy rate. Indeed, it tells me that it is prudent to hold this rate at its current restrictive stance perhaps for longer than previously thought to help keep inflation on a sustainable trajectory toward 2 post: FED'S WALLER/ECNY: RISK OF WAITING TO CUT RATES 'IS SIGNIFICANTLY LOWER THAN ACTING TOO SOON' #Waller #FederalReserve post: #Fed 's Waller -Data warrants fewer cuts or later start to easing. -Rate cuts appropriate this year but not yet. -Need a couple more months of better inflation data to cut -Risk of waiting to cut is lower than acting too soon. $USD post: MORE FED'S WALLER/ECNY: SKEPTICAL THAT IMPROVEMENTS IN PRODUCTIVITY GROWTH WILLL BE SUSTAINED SO THAT LEVEL OF PRODUCTIVITY CAN KEEP RISING #Waller #FederalReserve

From youtube.com/markets|Mar 27, 2024

From youtube.com/markets|Mar 27, 2024Today is the anniversary of Silver. Thursday, March 27th, 1980, the day the billionaire Hunt brothers met their comeuppance after trying to corner the commodities market. It was ...

- Story Stats

- Posted: Mar 27, 2024 4:50pm

- Submitted by:Category: Fundamental AnalysisComments: 0 / Views: 140