Following a slow end to 2023, a slow start to 2024

Insight

The sell-off in global bonds continued with fresh cycle highs being set for longer-term yields. The

US: ISM manufacturing, Sep: 49.0 vs. 47.9 exp.

EA: Unemployment rate (%), Aug: 6.4 vs.6.4 exp.

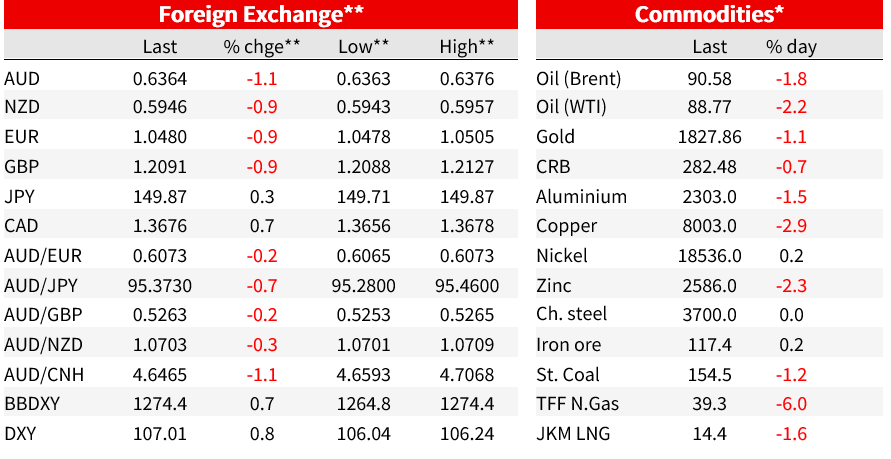

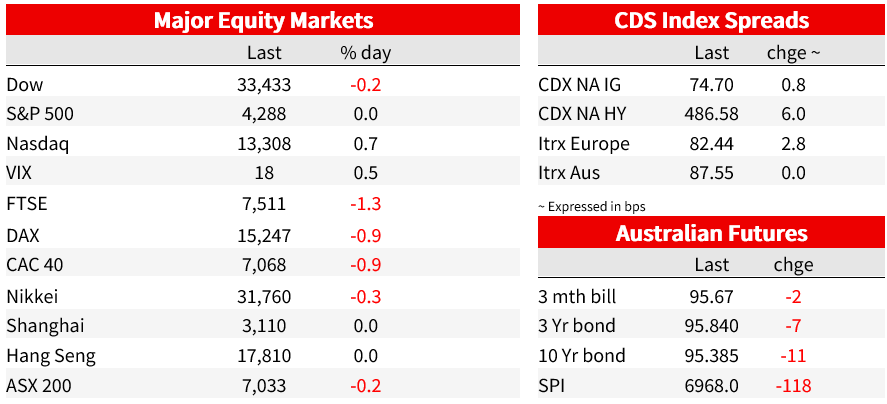

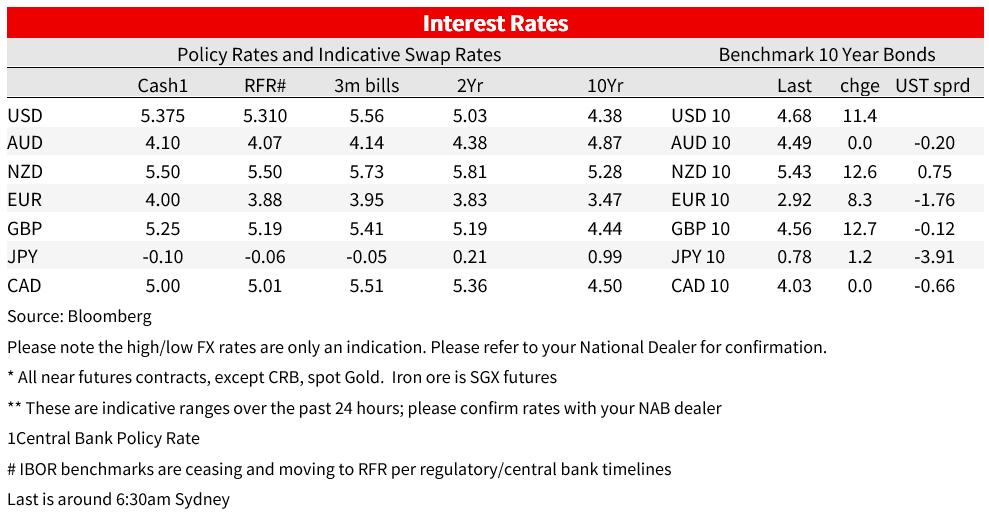

The sell-off in global bonds continued with fresh cycle highs being set for longer-term yields. The US 10yr yield hit 4.70%, up some 12bps and currently trades at 4.69%. Weekend news of a surprise last-minute agreement by Congress to avoid a US shutdown saw yields open higher on Monday (the bill extends spending through to 17 November). Those moves extended overnight. BoE MPC member Mann came out hawkish, seeing Gilt yields higher. And the Fed’s Bowman also repeated “further rate increases ” are needed. A beat in the US ISM Manufacturing added to moves (49.0 vs. 47.9 expected). Fed Funds pricing shifted higher with around a 50% chance of another rate hike by December, up from 39% on Friday (terminal now 5.46% from 5.43%). Equity markets are mixed with the S&P500 -0.0%, but NASDAQ +0.7%. The lift in yields and ongoing US data resilience has seen the USD lift back to 2023 highs.

First to the US ISM Manufacturing. The headline index beat expectations at 49.0 vs. 47.9 expected and 47.6 previously. The key new orders (49.2 from 46.8) and employment (51.2 from 48.5) indexes rose strongly. Interestingly the prices paid index fell to 43.8 from 48.4, despite the recent rise in energy prices. Anecdotes within the survey were very mixed, though tended to lean towards stabilisation – one firm noted “overall, things continue to be very steady: Sales and revenue are as expected, and the supply environment has stabilized greatly versus 2021-22”. As for the agreement that avoids a US shutdown, Congress has set itself a new deadline of 17 November, but expect more protracted fights (see WSJ: Congress Stopped a Shutdown, but Fights on Ukraine, Border Intensify).

As for BoE MPC member Mann, she noted that: “I believe the Monetary Policy Report forecast for a long time has been telling a story fundamentally different from the ones that I consider likely,” and that “My story has been one of more resilient domestic demand and more persistent price pressures, which therefore requires a more restrictive monetary policy stance ”. Her inflation forecasts are at the upper end of the BoE’s fan charts for inflation projections, meaning she is likely to continue to argue for further hikes. As for the higher for longer narrative that has been driving markets recently, Mann said that policy makers are facing a “world where inflation shocks are likely to be more frequent” with stronger price growth meaning interest rates will need to be permanently higher.

Mann’s hawkish comments saw UK Gilt yields rise, which added to the lift in global yields. The UK 10yr yield was up 12.7bps to 4.56%, the German 10yr up 8.3bps to 2.92% and Japan’s 10-year rate reached a fresh decade-high of 0.78% yesterday. The BoJ announced it would purchase extra amounts of 5-10 year debt on Wednesday to contain yields. Higher oil prices haven’t contributed to the rates backdrop, with prices down for the third day running, currently down 2-2½ for the day, WTI at 88.61 and Brent crude below 90.49. That’s also reflected in the US 10yr implied inflation breakeven which was broadly steady at 2.34%. The moves in nominals continues to be reflected in real yields with the 10yr TIP yield +10.4bps to 2.34%.

US Fed speakers mostly repeated existing points. The Fed’s Bowman re-iterated it will likely be appropriate to raise rates further and hold them at restrictive level for some time. In contrast Vice Chair for Supervision Michael Barr said the US central bank is “likely at or very near” a level of interest rates that is sufficiently restrictive and that the bigger question is how long rates will need to stay high, adding that the full effects of past increases on the economy “are yet to come in the months ahead.” Chair Powell also spoke, but kept pretty close to script, noting in a good labour market that lasts for a sustained period of time “ more and more of the wage needs actually go to people at the lower end of the wage spectrum,” “These are really beneficial things. To have that, though, the record is also clear that we need price stability,”

In FX, weaker risk sentiment and US data outperformance has seen broad-based support for the USD , with the DXY index recovering losses at the end of last week to punch back up through the recent high to just shy of 107 (+0.7% to 106.99). The Yen fell to a fresh low for the year, but USD/JPY has stopped short of the 150 mark, trading just below that psychological level, a break of which would raise the chance of official intervention. EUR is back trading sub 1.05 and GBP is holding just over 1.21. The AUD is very weak, down -1.1% to 0.6366. Ditto the NZD -0.9% to 0.5946. Chinese PMI data on the weekend was mixed. The official versions had slight beats (manufacturing 50.2 vs. 50.1e; non-manufacturing 51.7 vs. 51.6e), but the Caixin versions missed big (manufacturing 50.6 vs. 51.2e; non-manufacturing 50.2 vs. 52.0e). Note China is out this week with Golden Week Holidays.

Coming up:

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Following a slow end to 2023, a slow start to 2024

Insight

Strong issuance volumes underpinned by extremely robust levels of investor liquidity and improved economic conditions.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.